Capital gains on selling a property and reinvestment

Although house prices in Luxembourg have fallen since 2022, investors who have owned their property since 2020 or earlier are still likely to realise capital gains on its sale. There are two questions for investors: how to minimise any tax on the capital gain, and how to reinvest the proceeds as efficiently as possible.

Sale of a non-taxable main residence compared with taxable property

Capital gains do not apply to your main residence in Luxembourg. However, if you sell a buy-to-let property or a holiday home, you may be liable for tax on any gains you make. In general, a property counts as a main residence, for the purposes of a sale, if you lived in the property at the time of the sale, or if the sale happens by December 31 of the year following relocation to your new main residence, provided you lived in this property immediately after its initial purchase, or completion, or for at least five years prior to the sale.

Taxation of properties that are not a main residence

The gain is the difference between the sale price and the original purchase price, less any acquisition costs, which include fees payable to real estate agents and notaries, and for registration and transcription.

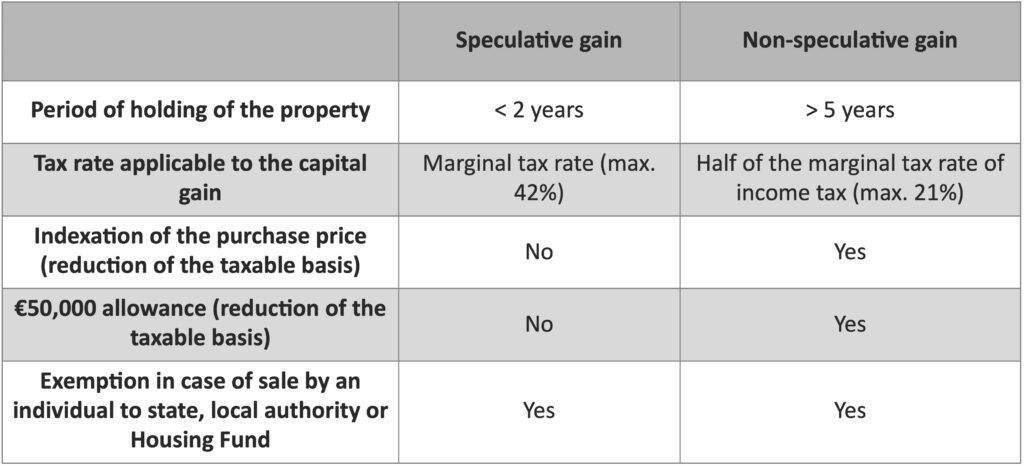

The timing of the sale is important, as it may impact the taxable basis and the applicable tax rate. If you have owned the property for five years or less, the profit is considered to be speculative.

In the event of a gain categorised as speculative, tax is levied at the individual’s marginal rate of income taxation, and could be as much as 42% for higher earners. In the case of non-speculative sales, the gain is classified as extraordinary income and taxed at a more favourable rate – half of the marginal rate.

Sellers in a non-speculative sale can claim an indexation allowance created to mitigate the impact of inflation. A coefficient is applied to the purchase price, depending on when the property was acquired. In these cases, sellers also benefit from a €50,000 allowance (double in the case of joint taxation) reducing the taxable basis, the capital gain.

In addition, exemptions from capital gains tax apply to sales of real estate by individuals to the state and local authorities, and to Luxembourg’s Housing Fund, the country’s public affordable housing promotion body, as long as the property is not subject to a right of pre-emption.

In addition, exemptions from capital gains tax apply to sales of real estate by individuals to the state and local authorities, and to Luxembourg’s Housing Fund, the country’s public affordable housing promotion body, as long as the property is not subject to a right of pre-emption.

This table sets out the taxation of capital gains on a property that is not your main residence:

This leaves two main options to homeowners who want to minimise their capital gains tax liability. The first is not to sell until you have passed the five-year threshold. The second is to wait until your income is lower, such as in retirement, when your marginal tax rate is likely to be lower.

Reinvesting the proceeds

An initiative introduced in 2024 is intended to expand Luxembourg’s stock of affordable housing and ease pressure on the rental market. The legislation offers so-called rollover relief from capital gains if a specific type of property is bought with funds obtained from the sale of a previous home (not a main residence) and does not qualify as speculative. The new property, to be acquired by 2027 under the legislation, must be classified as a social rental property, or fall into the A+ class for energy efficiency, thermal insulation and environmental performance.

Social rentals, which aim to provide affordable housing for lower-income households, are overseen by organisations designated by the Housing Ministry under rules that came into effect in 2009. Rents must be lower than the market rate, which would be a consideration for a landlord making a new investment. Its advantages include that the rent is guaranteed by the state, the tenants are supervised, and there is financial assistance with property maintenance.

Owners also benefit from tax exemptions. The rules introduced in 2024 exempt rental income from social rental management organisations from tax by up to 90%, up from 75% previously. The capital gains tax rollover relief means the gain is deferred rather than creating a permanent exemption, but it offers some flexibility on timing, enabling sellers to postpone recognising the capital gain until their tax rate is more favourable.

Impact on the housing market

The new rules are likely to make energy-efficient buildings more valuable and depress the market for energy-intensive properties, making it more difficult to sell property that does not meet energy efficiency standards and regulatory requirements.

This has already been seen in other countries – in France, for example, there is a ban on renting out the least energy-efficient properties, and the efficiency criteria are expected to be raised progressively over the next decade. This may increase the value of investment in the energy performance of a property to be rented or sold, including measures such as the enhancement of insulation and the modernisation of heating systems that should save money in the longer term.

The new rules may also help stimulate a revival of Luxembourg’s housing market by creating new incentives for investors. The market, which has been in decline since the fourth quarter of 2022 after a long period of expansion, started to recover in 2025 but remained depressed at the end of that year. The rules on capital gains for social housing were introduced as part of a package of measures to stimulate the market, including rental allowances for under-30s.

For property owners, the new rules increase options when it comes to selling, particularly useful for people who have owned a property for a long period and have accumulated significant potential capital gains. The incentives for deploying capital in social rental housing are attractive, although landlords also need to be comfortable with the risks. Nevertheless, taxation has a significant overall impact on the property market that homeowners should consider.

Mortgage

Mortgage Personal loan

Personal loan Savings

Savings